Understanding Moving Insurance: Protecting Your Belongings with Comprehensive Coverage and Claims Support

Moving insurance is the financial protection that covers damage, loss, or theft of household goods during a relocation, and it bridges the gap between a mover’s limited valuation liability and full replacement value provided by insurers. This guide explains why moving insurance matters, outlines the main coverage types—released value, full value, and third-party policies—and walks you through choosing coverage, protecting fragile items, and filing claims. Many households underestimate transit risks: a single damaged antique or a cracked TV can cost more than basic carrier liability will cover, leaving families responsible for repair or replacement costs. This article provides clear definitions, practical examples, and step-by-step guidance so you can decide what level of protection fits your move. Read on to learn how different valuation and insurance options work, compare coverage with a concise table, review actionable packing and documentation advice, and see how an example mover’s protections and claims workflow operate in practice.

What Is Moving Insurance and Why Is It Essential?

Moving insurance is coverage that pays to repair, replace, or settle for belongings damaged or lost in transit, and it functions by assigning a declared or default value to items and attaching remedies when perils occur. This protection reduces out-of-pocket risk from common moving incidents such as accidental drops, vehicle mishaps, and handling damage, delivering both financial replacement and peace of mind. For movers and shippers, moving insurance acts as a risk transfer mechanism: either the carrier accepts limited valuation liability or a licensed insurer underwrites a broader policy. The practical result is that households can choose protection that aligns with the replacement cost of their goods and their risk tolerance. Understanding how coverage differs and how claims are resolved helps you select the right option for everything from low-value boxes to irreplaceable family heirlooms.

How Does Moving Insurance Safeguard Your Valuables During Relocation?

Moving insurance safeguards valuables by providing three primary remedies—repair, replacement, or cash settlement—triggered when covered perils result in loss or damage; insurers assess the loss and apply the appropriate remedy based on policy terms. Typical perils include accidental damage during loading/unloading, transit collisions, and theft, while exclusions often cover improper packing, normal wear and tear, and certain high-value items unless declared. When a claim is approved, an insurer or carrier arranges repair services, sources replacement items, or issues a cash payment based on declared or replacement value formulas. Documenting condition, retaining damaged packaging, and filing promptly are essential steps that speed resolution and maximize recovery under policy terms. These practical safeguards reduce the financial shock from moving incidents and make recovery predictable.

What Is the Difference Between Valuation Coverage and Moving Insurance?

Valuation coverage is the mover’s legal liability framework that limits carrier payout per pound or per item, whereas moving insurance refers to a third-party policy underwritten by a licensed insurer that can offer replacement-cost protection and broader perils. Under valuation, carriers commonly calculate compensation using a per-pound rate for lost or damaged goods, which often yields modest payouts that do not reflect replacement cost; by contrast, moving insurance can cover repair, replacement, or full cash settlement up to declared values. The distinction matters because a valuation-based payout for a damaged high-end television or an antique dresser may be far lower than the cost to repair or replace the item. Comparing an example calculation—per-pound valuation versus declared replacement value—illustrates why many consumers opt to declare value or buy third-party insurance for higher-value shipments.

What Are the Main Types of Moving Insurance Coverage?

The three primary coverage options for household moves are Released Value Protection, Full Value Protection (carrier valuation upgrade), and Third-Party Moving Insurance, each differing in calculation method, scope, and cost. These options form a hierarchy from minimal, low-cost protection to comprehensive, higher-fee policies that more closely mirror replacement value. Knowing the strengths and limits of each type helps you match coverage to shipment value and risk. Below is a quick list of the types and what they generally mean.

- Released Value Protection: The carrier’s default, low-cost option that limits liability to a nominal per-pound rate.

- Full Value Protection: An upgraded carrier valuation where the mover agrees to repair, replace, or provide cash settlement up to declared value.

- Third-Party Moving Insurance: Policies sold by licensed insurers that cover a wider range of perils and often pay replacement cost subject to policy limits.

| Coverage Type | Coverage Characteristic | Typical Payout Example |

|---|---|---|

| Released Value Protection | Per-pound limited liability provided by carrier | $0.60 per pound for damaged items (low payout) |

| Full Value Protection | Carrier repairs, replaces, or pays cash up to declared amount | Repair or replacement of a damaged sofa up to declared amount |

| Third-Party Moving Insurance | Insurer underwrites replacement-cost or broadened perils | Replacement-cost payout for antique after appraisal |

What Is Released Value Protection and What Does It Cover?

Released Value Protection is the mover’s baseline liability coverage that compensates you based on a per-pound rate for lost or damaged items, and it is typically free or included in standard service. Because compensation is weight-based, high-value but lightweight items—such as electronics, jewelry, and artwork—are poorly served by this approach; payouts often fall short of replacement cost. Exclusions commonly include items not properly packed by the customer, naturally deteriorating goods, and certain high-value items unless declared. Choosing released value is appropriate for low-risk shipments of common household goods where replacement cost is modest and risk tolerance is higher. For irreplaceable items or shipments with a high total declared value, released value protection is often insufficient.

How Does Full Value Protection Provide Comprehensive Coverage?

Full Value Protection is an upgraded carrier valuation in which the mover accepts responsibility to repair, replace, or provide a cash settlement for lost or damaged items up to a declared value, making the coverage closer to replacement-cost protection in practice. Customers typically pay a fee or percentage based on the declared shipment value, and the declared value determines maximum recovery for each item or the shipment as a whole. This option addresses the primary limitation of released value by tying recovery to declared monetary worth rather than weight, which protects lightweight but costly items. For homeowners moving expensive furnishings or electronics, full value protection is often the recommended balance between cost and security.

When Should You Consider Third-Party Moving Insurance?

Third-party moving insurance should be considered when you need broader perils coverage, higher limits, or replacement-cost payouts that exceed carrier valuation options, and when moving high-value, collectible, or hard-to-replace items. Licensed insurers can provide policies that cover acts of God, additional transit risks, and higher coverage ceilings, subject to terms and exclusions, and they are useful when carrier options leave coverage gaps. Before purchasing, verify the insurer’s credentials, review policy terms for exclusions and deductibles, and obtain appraisals for antiques or jewelry that may need scheduled coverage. Third-party insurance is particularly prudent for interstate, long-distance moves or commercial relocations where replacement costs and exposure are higher.

What Protection Options Does Your Hometown Mover Offer?

Your Hometown Mover provides a set of liability and service features designed to make protection choices straightforward while offering trust signals that help customers decide on upgrades and documentation needs. The company emphasizes an Easy Claims Process and maintains Licensed & Insured status, offering Certificates of Insurance (COI) provided upon reservation for customers who require proof of coverage. Additionally, the mover promotes the MoveMatch Guarantee for competitive pricing and flexible payments including “Move Now, Pay Later w/ 0% APR.” These customer-facing assurances pair with trust indicators—a USDOT#: 2789843, MC# 045842, NYDOT# 39744, an A+ BBB rating, and over 400 5-star reviews—that support reliability in both residential and commercial moves. Below is a short list summarizing what customers can expect when selecting protection options with this company.

- Free basic liability included for standard service (see details below).

- Upgrade paths available to increase coverage via declared value or purchased comprehensive options.

- COI and documentation provided at reservation for business and regulated moves.

Beyond liability and valuation, Your Hometown Mover also offers practical solutions to streamline your relocation, including efficient junk removal services to help declutter your space before or after your move.

What Are the Free Basic Liability Coverage Terms for Local and Long-Distance Moves?

The mover’s free basic liability provides differing baseline terms for local moves versus long-distance moves, and customers should interpret these terms as minimal protection included with many standard quotes. For local moves the company provides complimentary basic liability coverage appropriate to short-haul service, and for long-distance moves it includes a baseline released value protection consistent with carrier valuation norms. While free basic coverage reduces immediate cost, practical implications include limited per-pound payouts and common exclusions that may leave higher-value items underinsured. Customers evaluating whether to accept free basic liability should compare the expected replacement cost of their goods to the likely carrier payout and consider upgrading or purchasing third-party insurance when replacement cost exceeds the free coverage ceiling.

How Can You Upgrade to Comprehensive Liability Coverage?

Upgrading to comprehensive liability with Your Hometown Mover involves declaring shipment value and selecting a higher-tier valuation or arranging third-party coverage at the time of reservation, and customers are advised to request a Certificate of Insurance when arranging upgrades for commercial or high-value moves. The process generally requires providing an inventory or declared value estimate during booking, choosing the desired coverage level, and confirming fees associated with higher declared value. Upgrades affect claims outcomes by increasing maximum recovery and often changing remedies from per-pound payouts to repair or replacement. Customers should document high-value items, request COI documentation as needed, and confirm coverage details before moving day to ensure expectations match policy terms.

How Do You Choose the Right Moving Insurance Coverage for Your Move?

Choosing the right moving insurance coverage begins with an accurate inventory and estimated replacement cost, then weighing distance, fragility, and personal risk tolerance to balance cost with protection. A practical decision framework includes assessing the shipment’s total declared value, identifying high-value items that need scheduled coverage, and deciding whether carrier valuation will suffice or if third-party insurance is required. This section provides a short checklist to guide the decision and help prioritize coverage purchases for typical household scenarios.

- Inventory and value: List items and estimate replacement cost for each high-value piece.

- Move distance and exposure: Prioritize higher coverage for long-distance and interstate moves.

- Item fragility and uniqueness: Schedule or insure antiques, artwork, and specialty electronics separately.

- Budget vs risk tolerance: Match coverage level to the financial risk you’re willing to retain.

What Factors Should Influence Your Coverage Decision?

Major factors shaping coverage choice include declared shipment value, move distance, the presence of storage in transit, and the fragility or uniqueness of individual items, and these influence both the type and level of protection you’ll need. Declared value determines maximum recovery under many full-value options, while distance and transport mode increase exposure to transit risks and potential perils. Storage periods—even short-term—may introduce separate coverage needs, so check whether coverage extends during storage or if supplemental storage insurance is required. Evaluating these factors together yields a prioritized protection plan: insure the highest-value and most fragile items first, then tailor overall shipment coverage to the remaining household goods.

How Should You Protect High-Value and Fragile Items?

Protecting high-value and fragile items combines choosing appropriate insurance with proactive packing, documentation, and specialist handling such as crating or white-glove services; this layered approach reduces claim frequency and substantiates loss or damage when it occurs. Professional crating, use of original boxes with adequate cushioning, and separate handling instructions reduce transit risk, while photographing items, keeping receipts, and obtaining appraisals provide the documentation insurers require. When values exceed carrier valuation limits, schedule items on declarations or purchase third-party policies that explicitly list covered perils and limits. These preparation steps lower the chance of damage and speed resolution if a claim is necessary.

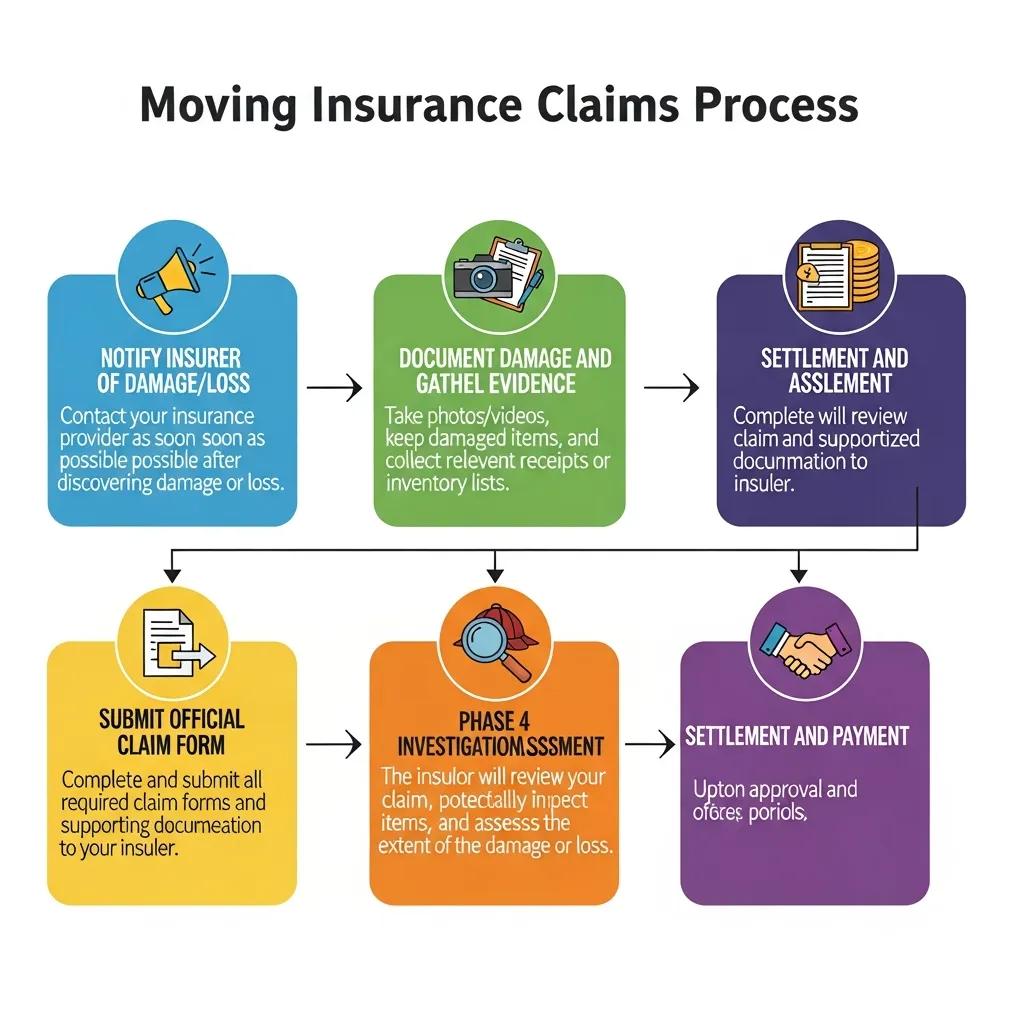

What Is the Step-by-Step Claims Process with Your Hometown Mover?

A clear, prompt claims workflow saves time and increases recovery likelihood; Your Hometown Mover emphasizes an Easy Claims Process that maps customer actions to documentation and timelines, making it straightforward to file and resolve claims. Best practice steps include immediate notification to the mover upon discovery of damage, detailed photographic evidence, retention of packing materials, and submission of an inventory and receipts. The company’s approach aligns with standard claims triage: acknowledge, investigate, evaluate, and settle, with COI issuance available when required for business or commercial claims. The table below maps each step to required documentation and expected customer actions to clarify how the process proceeds in practice.

| Claim Phase | Required Documentation | Customer Action |

|---|---|---|

| Notify | Brief incident description, date/time | Report damage immediately upon discovery |

| Document | Photos of damage, original packaging, inventory | Photograph items and keep packaging for inspection |

| Submit Claim | Inventory list, receipts, appraisal (if applicable) | Submit documentation and declared values promptly |

| Investigation | Carrier/insurer inspection notes | Cooperate with inspection and provide requested info |

| Settlement | Repair estimates, replacement invoices | Accept repair, replacement, or cash settlement as offered |

How Do You File a Moving Insurance Claim?

Filing a claim requires immediate action: notify the mover as soon as damage or loss is discovered, gather photographic and documentary evidence, and submit a formal claim with the required inventory and proof of value. Follow these numbered steps to file effectively.

- Notify the mover promptly with a concise incident summary and date.

- Photograph all damaged items, include contextual shots of packaging and surroundings.

- Retain all packing materials and original receipts or valuations for high-value items.

- Submit an itemized inventory and supporting documents as requested by the mover or insurer.

- Cooperate with inspections and respond to follow-up requests to speed adjudication.

What Documentation Is Required for Damage or Loss Claims?

Claims require a clear set of documents—an itemized inventory, proof of value such as receipts or appraisals, dated photos showing pre- and post-move condition, and any COI if coverage was provided through reservation—to substantiate loss and facilitate payment.

Additional helpful records include repair estimates, police reports for theft, and correspondence related to packing instructions or known pre-existing damage. Missing or incomplete documentation is a common cause of claim delays, so assembling a dossier before filing is prudent. Providing complete, organized proof reduces friction during investigation and demonstrates the reasonableness of the requested settlement.

What Are Common Questions About Moving Insurance Costs and Coverage?

Cost and coverage questions center on how premiums are calculated, what factors drive price, and whether insurance is a worthwhile investment; clear answers help consumers budget and choose appropriate protection.

- Declared value: Higher declared values increase cost proportionally.

- Coverage type: Third-party policies and full value upgrades cost more than released coverage.

- Distance and mode: Long-distance moves generally attract higher coverage fees.

- Special services: Crating, climate control, and white-glove handling add to overall insurance cost.

| Pricing Factor | How It Affects Cost | Sample Range / Note |

|---|---|---|

| Declared Value | Directly proportional; higher declared value = higher fee | Fee often a percentage of declared value |

| Coverage Type | Third-party or full-value costs more than released value | Per-pound vs percentage or flat fee models |

| Distance | Longer moves raise exposure and cost | Interstate moves typically cost more than local |

| Special Handling | Crating/appraisal increases premium | Add-on fees for unique items |

How Much Does Moving Insurance Typically Cost?

Moving insurance cost varies by model: released value is often free or nominal, full value is typically charged as a percentage or flat fee based on declared shipment value, and third-party policies are priced based on risk, limits, and deductibles; sample calculations help illustrate typical ranges. As a rule of thumb, full value upgrade fees scale with declared amount and third-party premiums reflect replacement-cost exposure and any special-item scheduling. When estimating cost, multiply an expected premium percentage by declared value or consult insurer rate tables; including special handling or appraisal fees will raise the total. Understanding these models allows you to trade off incremental insurance expense against potential out-of-pocket replacement costs after a loss.

Is Moving Insurance Worth the Investment?

Moving insurance is worth the investment when potential out-of-pocket replacement costs exceed the premium and when you are transporting high-value, fragile, or sentimentally important items that would be difficult to replace. For low-value local moves, released value may suffice, but for long-distance relocations or shipments containing antiques and electronics, upgraded valuation or third-party policies usually provide better financial protection and peace of mind. A simple decision rule is to compare the total premium to the likely replacement cost of the most valuable items; if the premium is small relative to replacement exposure, purchasing higher coverage is prudent. Practical cost-reduction strategies include insuring only high-value items separately and using professional packing to minimize claim likelihood.

This final guidance helps you balance budget and exposure and, if desired, arrange upgrades or COI documentation with a mover that provides transparent options and a clear claims pathway such as those described above for Your Hometown Mover.

Frequently Asked Questions

What Should You Do If Your Items Are Damaged During the Move?

If your items are damaged during the move, the first step is to notify your mover immediately upon discovering the damage. Document the incident by taking clear photographs of the damaged items and their packaging. Retain all packing materials and any receipts or appraisals for high-value items. Then, follow the mover’s claims process, which typically involves submitting an inventory list and any required documentation. Prompt action and thorough documentation can significantly enhance the likelihood of a successful claim resolution.

Can You Purchase Moving Insurance After the Move Has Started?

Generally, moving insurance must be purchased before the move begins, as it covers risks associated with the transportation of your belongings. Once the move is underway, it is typically too late to secure coverage for items already in transit. However, some third-party insurers may offer policies that cover items during the move, but these are less common. It’s advisable to arrange for insurance well in advance to ensure adequate protection for your belongings throughout the entire moving process.

How Do You Determine the Declared Value for Your Items?

Determining the declared value for your items involves assessing the replacement cost of each item you plan to move. Start by creating an inventory list that includes high-value items, antiques, electronics, and any other possessions that would be costly to replace. Research current market values or obtain appraisals for particularly valuable items. The declared value should reflect the total cost to replace these items in the event of loss or damage, ensuring that you have adequate coverage during your move.

What Are the Exclusions in Moving Insurance Policies?

Moving insurance policies often contain exclusions that limit coverage for certain types of damage or loss. Common exclusions include damage due to improper packing, normal wear and tear, and specific high-value items unless they are declared and insured separately. Additionally, acts of God, such as natural disasters, may not be covered under standard policies. It’s crucial to read the policy details carefully and understand what is and isn’t covered to avoid surprises during the claims process.

How Can You Ensure a Smooth Claims Process?

To ensure a smooth claims process, start by notifying your mover as soon as you discover any damage or loss. Document everything meticulously, including taking photographs of the damage and retaining all packing materials. Submit your claim promptly along with an itemized inventory and any required receipts or appraisals. Familiarize yourself with the claims process outlined by your mover, and be prepared to cooperate with any inspections or follow-up requests. Clear communication and thorough documentation are key to expediting your claim.

What Should You Look for in a Third-Party Moving Insurance Policy?

When considering a third-party moving insurance policy, look for coverage that offers a broad range of perils, including theft, accidental damage, and natural disasters. Check the policy limits to ensure they meet your needs, especially for high-value items. Review the exclusions carefully to understand what is not covered. Additionally, consider the insurer’s reputation, customer service, and claims process efficiency. A policy that provides clear terms and responsive support can make a significant difference in your overall moving experience.

Conclusion

Understanding moving insurance is crucial for protecting your belongings during a relocation, as it offers financial security against loss or damage. By selecting the right coverage—whether it’s released value, full value, or third-party insurance—you can ensure that your high-value items are adequately protected. Take the time to evaluate your options and choose a policy that aligns with your needs and risk tolerance. For more information on how to safeguard your move, explore our comprehensive resources today.